matdesign24/iStock via Getty Images

PaySign, Inc. (NASDAQ:PAYS) continues to deliver double digit net sales growth driven by successful investments in prepaid card-based payment solutions targeting the plasma donation industry. With 465 plasma centers and 6.4 million cardholders as well as sponsorship with large banks and card companies, I believe that operating margin and FCF could grow in the coming years. In addition, the recent acquisition of shares by PaySign may accelerate the demand for the stock and lower the cost of capital. There are clear risks coming from change in the regulatory framework, lower net sales growth than expected, or failed partnerships. With that, I think that PAYS could trade a bit more expensively.

PaySign

PaySign is a North American company that offers prepaid card services and processing services for corporate, institutional, and individual clients. These two services are the main sources of income for the company. Taking into account that processing services are used by public institutions for the organization of their internal accounts and private consumers to save costs and processing times, they do not mean greater income for the company, rather they are one of the tools the company has to generate loyalty and recognition, with the aim of getting them to contract one of the prepaid card products.

Products include gift cards, corporate benefits, reloadable debit cards, medical or pharmaceutical assistance, donations, compensation, and withdrawing money from savings accounts. The company is currently seeking to expand its product offering towards travel cards and services related to them.

The business of the company is organized via a single segment, with domestic reach within the United States. Open-Loop Prepaid Card Market Forecast has long-term growth forecasts, with an annual rate of 8% between 2024 and 2027, reaching a capitalization of around $836 billion this year. In this regard, it is worth noting that other experts believe that the global prepaid card industry could grow at a CAGR of 19.5% from 2023 to 2032.

According to the report, the global prepaid card industry generated $2.5 trillion in 2022 and is anticipated to generate $14.4 trillion by 2032, witnessing a CAGR of 19.5% from 2023 to 2032. Source: Allied Market Research

PaySign’s products have been used by large companies listed in the Fortune 500 as well as other multinationals and pharmaceutical companies. By the end of 2023, company had 6.4 million customers, with at least one prepaid card activity, in more than 600 different offer programs.

The sales channels are managed by the same company. Due to the type of offer that the company has, its relationship with pharmaceutical companies is essential. Moreover, the offer of affordable prices for clients who target this sector is also very essential.

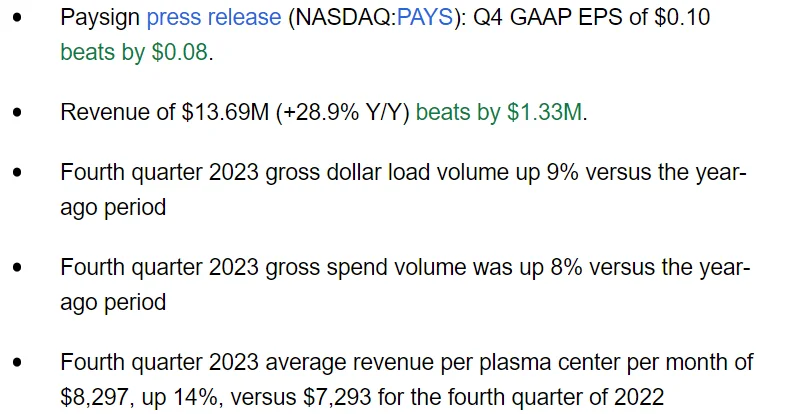

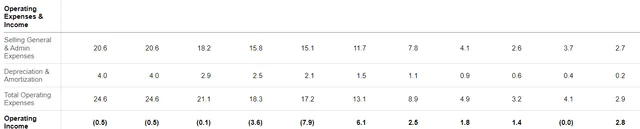

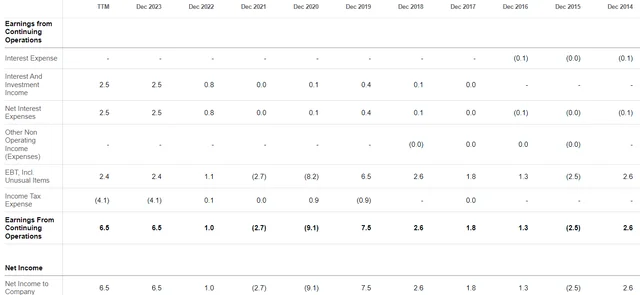

With that about the business model, I believe that it is worth having a look at the recent quarterly figures, which included better than expected EPS and quarterly net revenue. It is also worth noting that the revenue per plasma center per month continues to increase as compared to the same figures in Q4 2022.

Source: Seeking Alpha

Balance Sheet

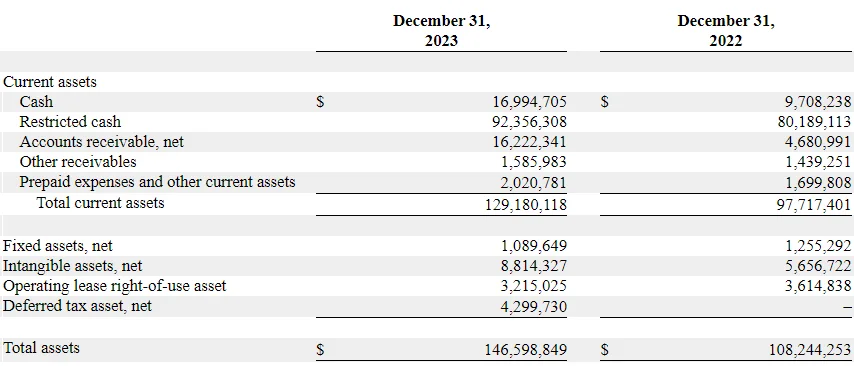

As of December 31, 2023, PaySign reported a stable balance sheet with a considerable amount of cash and current ratio larger than 1x. Besides, the asset/liability ratio was also larger than 1x. The company reports restricted cash worth $16 million, which is the money received from prepaid card holders. I did not take into account the restricted cash for the calculation of the enterprise value.

Source: 10-k

PaySign reports a significant amount of intangibles, so I had a look at what they represent. Most of intangibles reported include assets related to the platform as well as customer lists and contracts. I believe that these are assets that the company acquired in the past. It is also worth noting that amortization of these assets appears significant. In particular, in 2023, accumulated amortization increased from close to $9 million to about $13 million.

Source: 10-k

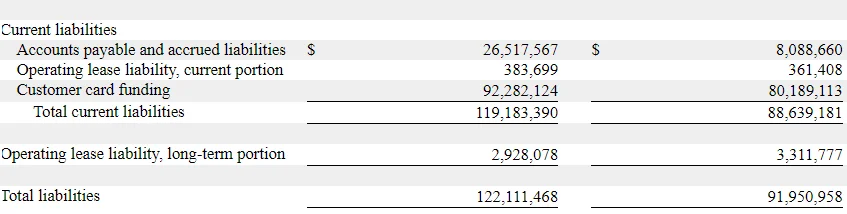

With regard to the list of liabilities, the most relevant is that PaySign does not show debt. Accounts payables and customer card funding seem enough to finance the operations of PaySign.

Source: 10-k

Hypothesis 1: Plasma Revenue Could Accelerate Net Sales Growth Under My Base Case Scenario

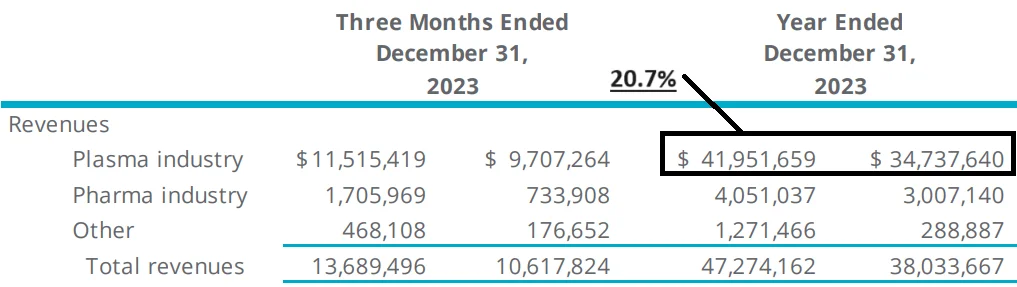

For the year 2024, the forecasts are positive for the company, with the expectation of reaching revenues close to $54.6 million and $56 million in annual rate, with a 100% increase in the pharmaceutical sector and also significant, although smaller, increase in the supply of plasma products. Given the recent increase in net sales growth in the Plasma industry, I believe that we could expect further momentum growth in the coming years.

In 2011, we began marketing a corporate incentive prepaid card-based payment solution targeting the plasma donation industry. Source: 10-k

Source: Quarterly Press Release

The company is expected to continue expanding its supply channels, as it did in 2023, obtaining positive results, from the opening of 465 new plasma centers and more than 20 programs for clients in the pharmaceutical sector. For this reason, as noted previously, the company’s relationships and investments in these areas are a cornerstone to continue sustained growth. In my view, the new plasma centers will most likely bring FCF acceleration and FCF margin growth.

Hypothesis 2: New Pharmaceutical Solutions Enhance Net Sales Growth, And Bring Economies Of Scale

I believe that further development of products for the pharmaceutical industry could also bring net sales acceleration and certain economies of scale. With money received from large corporations in the pharmaceutical company, I think that the number of products offered could grow in the coming years.

Let’s note that right now the company does not only offer prepaid cards, but also client call center service and support, pharmacy claims adjudication, and CRMs. Under my base case scenario, these new products may bring median net sales growth of about 10.8%.

Funds are provided by the sponsoring pharmaceutical company for use at retail pharmacies, specialty pharmacies, hospitals, doctors’ offices and clinics nationwide. Source: 10-k

Our offerings also allow clients to directly manage more of their pharmacy benefits and include pharmacy claims adjudication, network and payment administration, client call center service and support, reporting, rebate management, as well as implementation, training and account management. Source: 10-k

Hypothesis 3: Sponsorship And New Partnerships With Banks Enhance Net Sales Growth And Operating Margin

PaySign obtains sponsorship from associated banking entities, and its income is derived from the various operations that include the offer of its services such as fees for use, commission charges in transactions, and management fees among others.

PaySign’s open-loop prepaid cards offer the possibility of integrating into the international network in which the main credit and card companies operate, such as Visa (V), Mastercard (MA), or Maestro, among others, offering a variety of possible uses. Furthermore, the use of this type of cards is increasing due to new phenomena in relation to physical and digital money, and it is a growing option for those people who do not have the requirements to open a bank savings account.Under my base case scenario, new partnerships with card companies and banks will most likely bring net sales growth and operating margin growth. As a result, under my base case scenario, I assumed a 2034 operating margin of about 9%.

Hypothesis 4: Repurchase Of Shares Leads To A WACC Of 6.7%

Given the recent acquisition of 394,558 shares of common stock for $1,127,884, I believe that demand for the stock could accelerate soon. Clearly, the fact that the company is buying shares at the current price marks means that there is some undervaluation in the stock.

Source: Seeking Alpha

On March 21, 2023, our Board authorized a stock repurchase program to repurchase up to $5 million of our common stock, subject to certain conditions, in the open market, in privately negotiated transactions, or by other means in compliance with Rule 10b-18 under the Exchange Act. The program is expected to be completed within 36 months from the commencement date. As of December 31, 2023 the Company repurchased 394,558 shares of common stock for $1,127,884 at a weighted average price of $2.86 per share. Source: 10-k

Under my base case scenario, I assumed that the demand for the stock could lower the cost of capital. As a result, I assumed a WACC of 6.7% in my base case scenario. In the worst case scenario, I included a WACC of 7.5%.

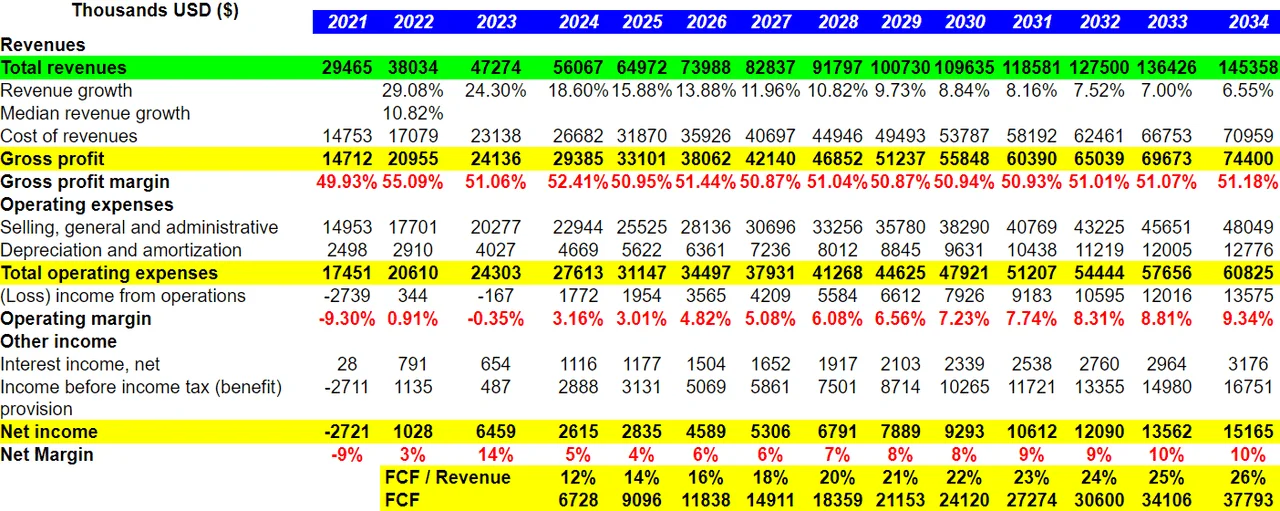

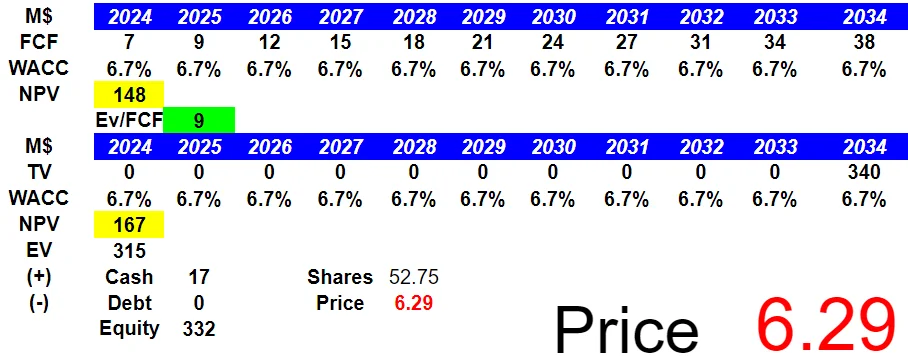

Base Case Scenario: Successful Hypotheses Lead To A Valuation Of $6.29 Per Share

Under my base case scenario, I assumed that the list of hypotheses was correct. As a result, the company reports net sales growth, operating margin growth, and significant FCF/net revenue growth. I also took into account previous figures reported by PAYS.

Source: Seeking Alpha

Source: Seeking Alpha

Source: Seeking Alpha

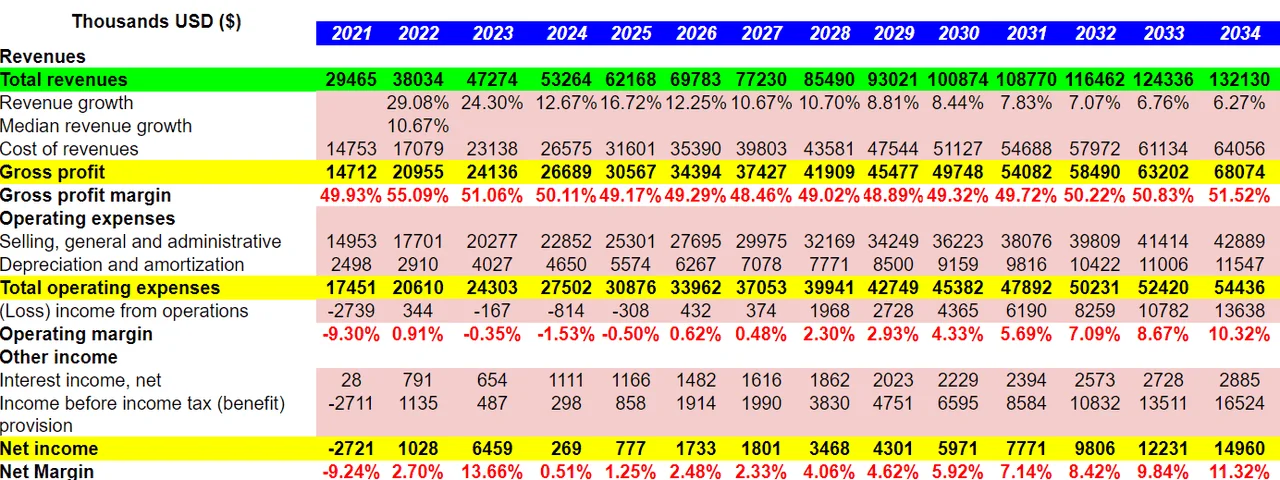

I included the following income statement items. First, 2034 total revenues would be close to $145 million, with cost of revenue worth $70 million and gross profit of $74 million.

In addition, with selling, general, and administrative expenses of $48 million as well as depreciation and amortization close to $12 million, total operating expenses stand at $60 million. The results would include income from operations of $13 million. Moreover, with interest income of $3 million, net income would be close to $15 million. Note that I assumed an operating margin between about 3% and 9% as well as net margin close to 10%.

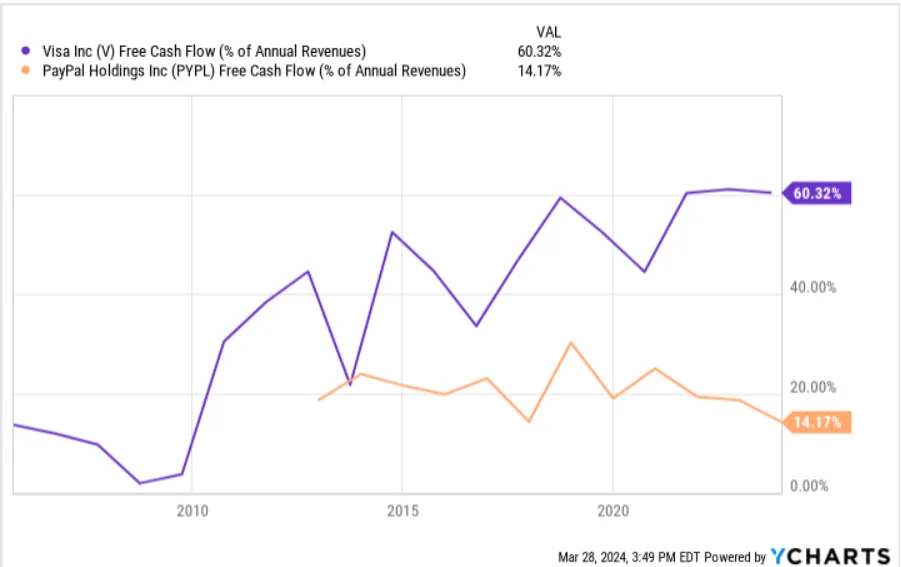

Finally, if we also include FCF/revenue close to 26%, revenue would stand at $37 million. Note that Visa (V) trades at close to 60%, and Paypal (PYPL) reports FCF/revenue of 14%. If PaySign continues to grow, I think that the company could be comparable to these large corporations. In my view, the FCF/revenue ratio close to 26% appears reasonable for a base case scenario. I also believe that my figures are conservative given the net sales reported in the most recent years.

Source: Ycharts

Source: My Expectations

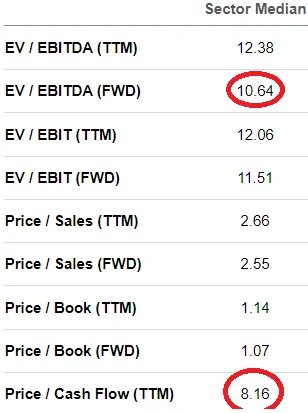

I assumed a WACC of 6.7%, which is in line with the cost of capital reported by other companies. In this regard, I would consult the following table offered by other analysts.

Source: Gurufocus

With EV/ TTM EBITDA in the sector of close to 10x and price/cash flow close to 8x, I assumed an EV/FCF ratio of about 9x. I believe that my figures are quite conservative.

Source: Seeking Alpha

My results would include enterprise value close to $315 million and an equity valuation of $332 million. Finally, the implied price would stand at about $6.29 per share.

Source: My Expectations

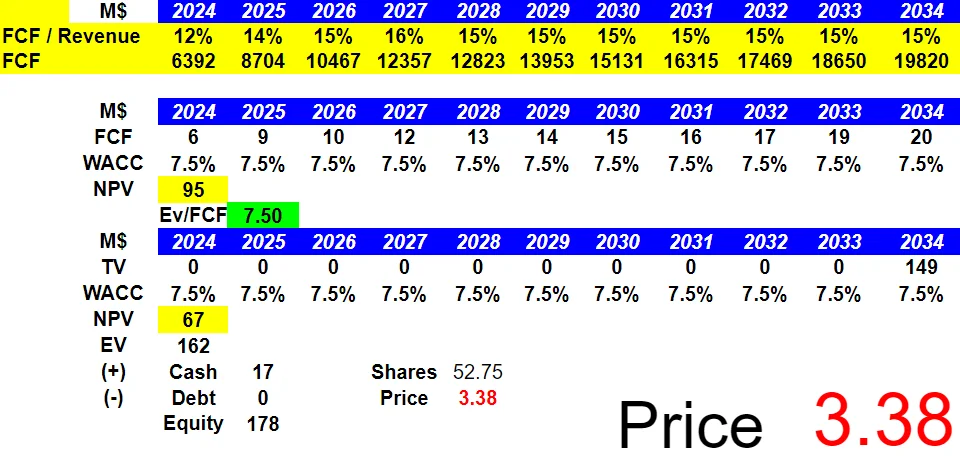

My Worst Case Scenario Includes Failure Of Hypotheses, Which Implied A Valuation Of $3.38 Per Share

My worst case scenario includes net sales growth, but the FCF/revenue is a bit lower than that in the base case scenario. Net income growth would also be lower than that in the previous case scenario. Finally, I include a WACC that is a bit higher than that in the previous case scenario. I assumed that lower demand for the stock could lead to increases in the cost of capital.

Under this scenario, I also included 2034 total revenues of $132 million, revenue growth of about 6.2%, and median revenue growth of about 10%. I also assumed a cost of revenue of about $64 million and gross profit close to $68 million.

In addition, I included selling, general, and administrative costs of $42 million, with depreciation and amortization of about $11 million. 2034 total operating expenses would stand at $54 million, and income from operations would be $13 million. Finally, with a 2034 operating margin of about 10%, interest income of $2.8 million, and income before income tax of $16 million, I obtained net income close to $14 million.

Source: My Expectations

If we assume a FCF/revenue ratio of 15%, 2034 FCF would be close to $19 million. In addition, with a WACC of 7.5% and terminal EV/FCF ratio of 7.5x, the implied fair price would stand at about $3.38.

Source: My Expectations

Competitors, And Risks

Within the market in which it participates, PaySign maintains minority positions compared to historical companies in the sector that have greater resources and market capitalizations. In some segments, such as payment solutions and pharmaceutical offerings, competition is highly fragmented, as there are several participants with specific products or regional reach. In addition to prepaid card companies, we must also consider banking entities with lines of credit and similar services as well as prepaid medicine and related companies.

Above and beyond competitive risks, it must be considered that any change in the regulatory frameworks within the markets in which the company participates could affect the current operation of the company. Within this, the growth objective and the forecasts could not reach the estimated values.

Of course, an economic crisis or reduction in the payment capacity of clients could reduce the demand for the company’s services, in addition to the evolution that exists in the markets for electronic media and digital tools for payment of services, which poses an innovation which could render the company’s current technological capabilities obsolete.

Conclusion

PaySign continues to deliver double digit net sales growth, and I believe that the recent 465 new plasma centers could accelerate growth in the coming years. In my view, management intelligently financed prepaid card-based payment solutions targeting the plasma donation industry. I also think that new sponsorship with large banks or card companies could bring additional FCF growth and operating margin growth driven by economies of scale and new potential clients. There are obvious risks coming from lower net sales growth than expected, changes in the regulatory framework, or failed partnerships with card companies. With that, I think that PaySign could trade a bit more expensive in the coming years.