Welcome back to the latest episode of The Future of Automotive on CBT News, where we put recent automotive and mobility news into the context of the broader themes impacting the industry.

I’m Steve Greenfield from Automotive Ventures, and I’m glad that you could join us.

This week’s lead story has to do with how autonomous vehicles could dramatically disrupt personal automotive insurance.

According to a brand new report from Morningstar, self-driving cars could make personal auto insurance largely obsolete within 20 years. A more likely, moderate scenario forecasts that personal insurance could remain necessary for a few more decades, until 2060.

The firm’s new report, called “Insuring Autonomy: Analyzing the Implications of Self-Driving Cars for the Auto Insurance Industry,” finds that by 2044, in the most aggressive adoption scenario, most cars on the road could be automated to a level where liability shifts from driver to the auto manufacturer. Morningstar believes that wide adoption of autonomous vehicles likely means that car insurance would be replaced by product liability insurance, which would ultimately be borne by the auto manufacturers when Level 4 or 5 autonomy is achieved.

Morningstar said the most important factors that will affect Automous Vehicle penetration rates are the timeline of technological development, pace of AV technology adoption and scrappage rate of the existing car fleet. The firm then developed three scenarios for each of these factors: very aggressive (the worst-case scenario for personal auto insurers), aggressive and moderate (the most likely scenario).

Morningstar noted that most vehicles currently in the market are at Level 2-3 automation, with driver assistance or navigation on autopilot systems like Tesla’s FSD Supervised. These systems can autonomously brake, accelerate, stop, steer, overtake, and change lanes in a complex urban or highway environment, but they still require continuous input from a human driver.

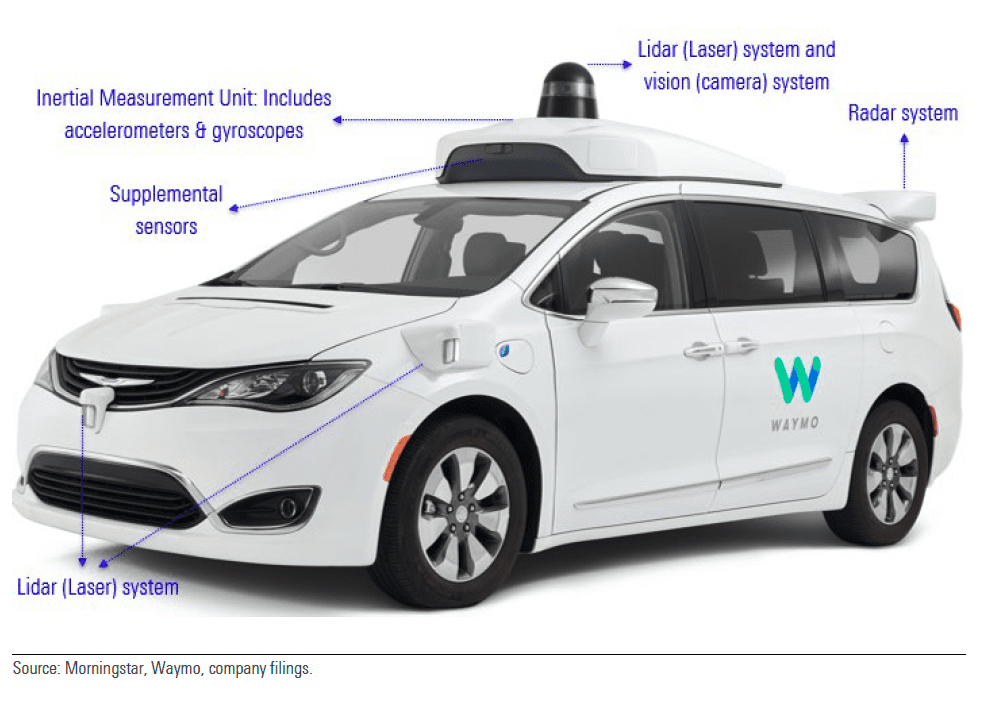

There are some Level 4 solutions from companies like Waymo or Cruise which offer robotaxis capable of driving without a human behind the wheel, but rides are currently limited to certain geographical locations where the software is trained extensively on location-specific parameters.

Using previous technologies as a guide, Morningstar calculates that Level 4 or 5 AV technology could reach an 80% adoption rate in as little as seven years (or 14 years with an aggressive scenario and 18 years with a moderate scenario).

Using these calculations, Morningstar projects that under its very aggressive, aggressive and moderate scenarios, 60% of the cars on the road will be Level 4 autonomous or higher by 2044, 2053 and 2060, respectively.

Morningstar assumes that the personal auto insurance won’t be affected significantly until Level 4 or higher autonomy is achieved at scale, when liability can be transferred from the driver to the auto manufacturer or the company that provided autonomous capability to the vehicle. This is because even in Level 3 autonomy, humans will have to take control in many conditions and can be held responsible in the case of an accident.

AVs are expected to begin having a material impact on auto insurance once a penetration rate of 10% is achieved (2035 in the very aggressive scenario). The business will decline at an increasing pace as the penetration rate increases from 10% to 60% (in 2043), at which point it stops creating any value and they expect that some of the vehicle insurance companies may be driven out of business.

So, with that, let’s transition to Our Companies to Watch.

Every week we highlight interesting companies in the automotive technology space to keep an eye on. If you read my weekly Intel Report, we showcase a company to watch, and take the opportunity here on this segment each week to share that company with you.

Today, our new company to watch is RueData.

RueData provides tire management software for transport fleets.

From a fleet perspective, tires represent the second most important item after fuel and that there is a general lack of tech tools to support their management.

RueData reduces tire consumption and maximizes the profitability of your fleet’s operating expenses.

RueData’s software has helped transportation companies save more than $3 million, positioning them as the #1 Tire Management Software in Latin America.

Fleets using the RueData product are experiencing some outstanding results, including:

- Reducing the purchase of new tires and saving up to 30% as a result.

- Identifying and reducing mechanical failures and tire theft.

- Saving up to 70% of time when conducting tire inspections.

- Getting optimized and automated maintenance plans within seconds.

- And, benefiting from technology that learns about the performance of your tires to increase their useful life.

Ruedata has helped transport companies save more than $1 million through their technology-based tire management software and data analysis.

If you’d like to learn more about RueData you can check them out at www.ruedata.com

So that’s it for this week’s Future of Automotive segment.

If you’re an AutoTech entrepreneur working on a solution that helps car dealerships, we want to hear from you. We are actively investing out of our DealerFund.

If you’re interested in joining our Investment Club to make direct investments into AutoTech and Mobility startups, please join. There is no obligation to start seeing our deal flow, and we continue to have attractive investment deals available to our members.

Don’t forget to check out my book, The Future of Automotive Retail, which is available on Amazon.com. And keep an eye out for my new book, “The Future of Mobility”, which is almost done, and will be out soon.

Thanks (as always) for your ongoing support and for tuning into CBT News for this week’s Future of Automotive segment. We’ll see you next week!