Counterpoint Research has revised down its 2025 global smartphone shipment growth forecast to 1.9 per cent YoY from the previous 4.2 per cent YoY, in light of the renewed uncertainties surrounding US tariffs.

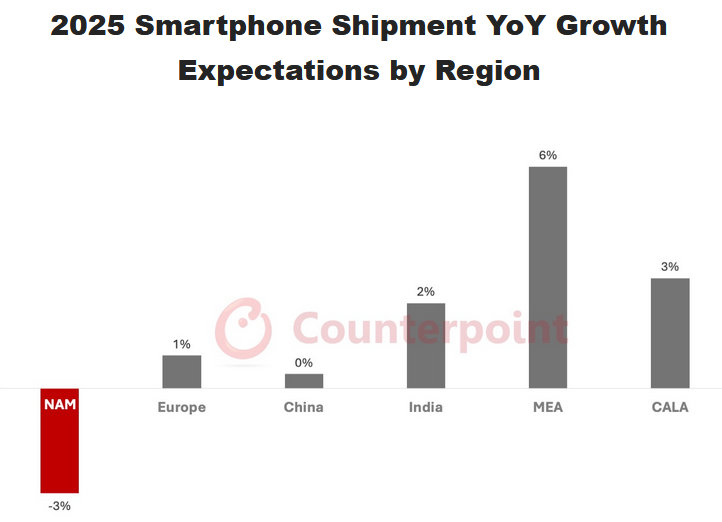

However, most regions will still likely see growth, except North America and China, according to Counterpoint Research’s Market Outlook Smartphone Shipment Forecast Report.

Price increases from cost pass-throughs remain a key focal point, although the tariff situation remains fluid and unpredictable.

Commenting on the revised forecast, Associate Director Liz Lee, say: “All eyes are on Apple and Samsung because of their exposure to the US market. Although tariffs have played a role in our forecast revisions, we are also factoring in weakened demand not just in North America but across Europe and parts of Asia.”

Lee added, “We still expect positive 2025 shipment growth for Apple driven by the iPhone 16 series’ strong performance in Q1 2025. Moreover, premiumisation trends remain supportive across emerging markets like India, Southeast Asia and GCC – these are long-term tailwinds for iPhones.”

Counterpoint Research’s current forecasts assume a relatively stable tariff environment through 2025, although the escalating rhetoric and uncertainty around trade policy could significantly impact OEM pricing strategies, supply chain planning, and, ultimately, consumer demand.

Commenting on projections for global smartphone shipment growth in 2025, Associate Director Ethan Qi said: “The bright spot this year – again – will likely be Huawei. We are seeing an easing around sourcing bottlenecks for key components at least through the rest of the year, which should help Huawei grab substantial share in the mid-to-lower-end segments at home.”

Qi added: “Is 2025 the breakout year for Huawei globally? It might be a bit soon for that but increasing supply chain strength will definitely help the brand establish a better foothold overseas in the medium term.”