Automotive OEM Telematics Market Size

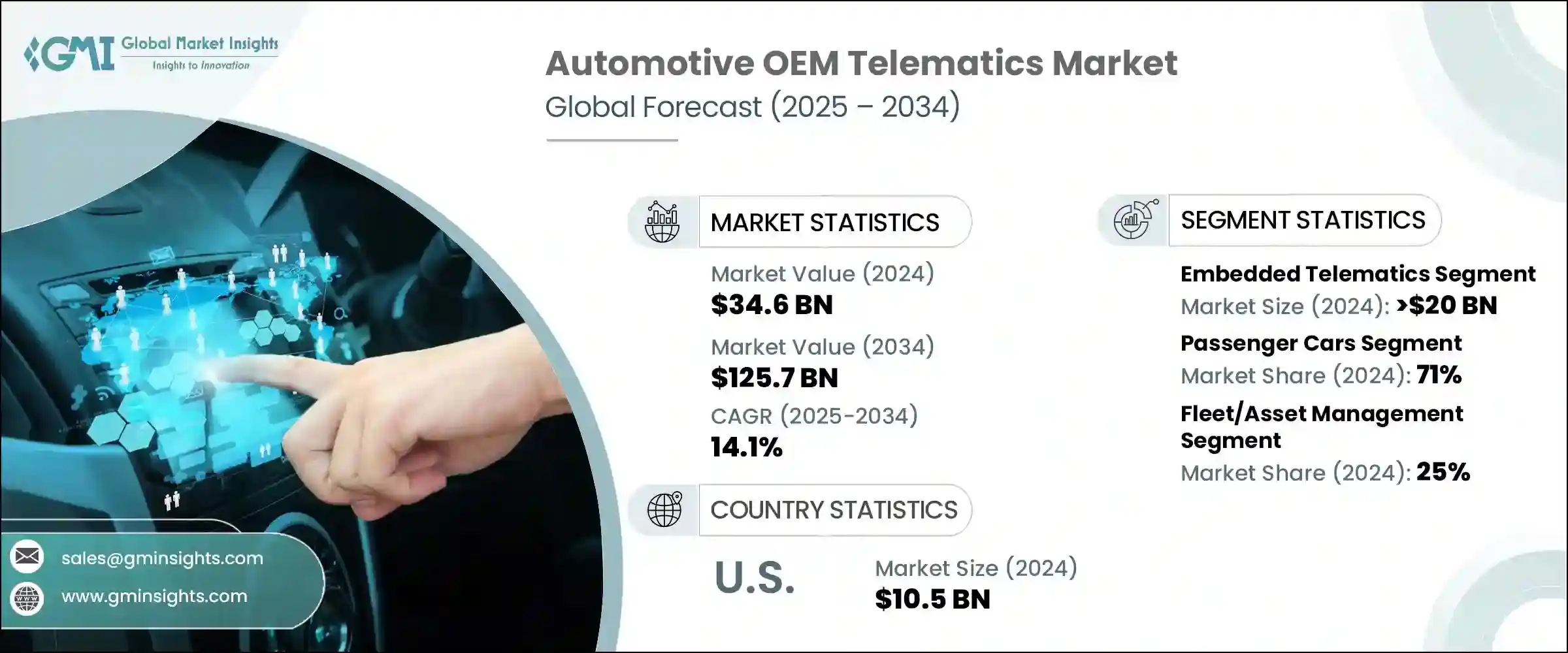

The global automotive OEM telematics market size was valued at USD 34.6 billion in 2024 and is estimated to register a CAGR of 14.1% between 2025 and 2034.

The rising consumer demand for connected vehicles equipped with integrated infotainment, navigation, diagnostics, and safety features is significantly advancing the OEM telematics market. As customers increasingly seek seamless digital experiences in their automobiles, such as real-time traffic updates, voice assistance, and remote vehicle controls, OEMS are integrating advanced telematics systems directly into their offerings. The advancement of smart mobility, along with the incorporation of smartphones and IoT devices in vehicles, is converting cars into interconnected platforms. This transition is encouraging automakers to innovate by making embedded telematics a standard feature that adds value.

Governments across major economies are mandating the inclusion of telematics systems in new vehicles to enhance road safety, enable emergency response, and support vehicle tracking. Regulations like the European Union’s E call mandate that all new vehicles be fitted with telematics systems that automatically notify emergency services in the event of severe accidents. Comparable legislation in nations such as Russia, India, and Brazil is driving OEMs to implement factory-installed telematics solutions. These regulations not only improve passenger safety but also promote wider acceptance by establishing a uniform expectation for connected safety technologies.

OEMs are progressively adopting telematics to generate new revenue streams through data-driven services. By offering fleet management solutions such as vehicle diagnostics, usage-based insurance, fuel efficiency monitoring, and predictive maintenance, OEMs focus on commercial vehicle operators and logistics companies. These services play a crucial role in enhancing operational efficiency and reducing costs, which makes them particularly attractive to automakers.

OEMs also benefit from fostering ongoing relationships with their customers and generating consistent income through subscriptions or cloud-based platforms. This movement towards service-oriented business models, made possible by telematics, is evolving automakers from standard vehicle suppliers into holistic mobility solution providers.

For instance, in February 2024, Ford Motor Company announced the growth of its Ford pro intelligence platform, which integrates improved telematics services for commercial fleet customers. This platform delivers real-time notifications about vehicle health, remote diagnostics, analytics on driver behavior, and predictive maintenance capabilities, all enabled by a cloud-based data infrastructure. The goal of this initiative is to improve fleet performance, reduce downtime, and provide subscription-based services specifically aimed at business customers. According to Ford, users of Ford Pro telematics have reported decreases in operational costs of as much as 20%.

Automotive OEM Telematics Market Trends

- Automobile manufacturers are increasingly selecting to integrate embedded telematics systems during the production phase, instead of depending on aftermarket solutions. This evolution offers automakers greater control over vehicle data, enhances cybersecurity and guarantees improved integration with other in-vehicle technologies. Embedded telematics also enable sophisticated features such as real-time navigation, predictive maintenance alerts, and over-the-air software updates. By incorporating these systems into new vehicle sales or leasing options, automakers can provide bundled services that improve customer satisfaction and cultivate long-term loyalty.

- Artificial intelligence significantly contributes to the evolution of automotive telematics. It enables real-time data analysis, predictive behavior modeling, and the creation of more personalized driving experiences. By leveraging AI, automakers and fleet operators can predict maintenance needs, decrease downtime, and enhance safety through a better comprehension of driver actions. This fosters innovations such as usage-based insurance and improved route planning. Vehicles generate vast quantities of data and are essential in transforming this critical data into actionable insights, which help deliver mobility solutions that are progressively responsive, intelligent and adaptable to evolving conditions.

- Vehicle-to-everything (V2X) technology is becoming a significant enhancement to modern telematics. It enables vehicles to establish connections not only with one another but also with road infrastructure, pedestrians and cloud networks. This form of communication is essential for the advancement of autonomous driving and the creation of smart cities. Automakers are progressively developing telematics systems that facilitate this, aiming to establish safer and more efficient transportation networks.

- The advantages are extensive, including accident prevention, traffic congestion reduction, and enhanced driver awareness of their environment. As international regulations advance, V2X is increasingly vital for compliance and will act as a fundamental component for future mobility solutions.

- For instance, in October 2023, Hyundai Motor Group revealed the successful rollout of its connected car navigation cockpit (CCNC), incorporating connected V2X telematics in particular models. This system allows for vehicle interaction with road infrastructure, offering improved route guidance and real-time traffic updates. Hyundai noted that these functionalities enable drivers to react more quickly to road dangers, thereby enhancing both safety and convenience, particularly in busy urban areas. The CCNC platform reflects Hyundai’s commitment to intelligent transportation systems that are in harmony with larger smart city projects.

Automotive OEM Telematics Market Analysis

")

Based on type, the automotive OEM telematics market is segmented into embedded telematics, tethered telematics and integrated smartphone telematics. In 2024, the embedded telematics segment held a market revenue of over USD 20 billion.

- Embedded telematics systems are becoming the preferred option for automotive OEMs because of their smooth integration, superior performance, and heightened security compared to aftermarket alternatives. These systems, which are built directly into the vehicle’s hardware, enable real-time data gathering, vehicle monitoring, remote diagnostics, and over-the-air (OTA) updates.

- OEMs favor embedded telematics because it allows them to have greater control over data and ensures better compatibility with proprietary platforms. As vehicles transition into software-defined entities, the need for deeply integrated telematics systems is growing, fueled by consumer demands for connectivity from the very first day of vehicle ownership.

- Global safety regulations are pushing the automotive industry toward embedded telematics, particularly for features such as E call (emergency call), vehicle crash notifications, and remote vehicle immobilization. In regions like the European Union, embedded telematics systems are now mandatory in new cars to ensure compliance with safety norms. In the Asia-Pacific and North America, governments are instituting mandates for vehicle tracking systems in fleet and commercial operations. These regulations are impacting OEM strategies, making embedded telematics a requirement for compliance rather than an additional premium feature, thus facilitating its wider adoption in mass-market vehicles.

- The integration of telematics within vehicles facilitates OEMs in adopting data-driven business models, which opens fresh revenue channels through options such as usage-based insurance (UBI), subscription-based infotainment, fleet management, and predictive maintenance. The persistent connectivity of embedded systems allows OEMs to sustain uninterrupted service delivery following the sale, thereby enhancing the lifetime value of customers.

- For instance, in May 2025, Toyota disclosed its plans to introduce Arene, a proprietary operating system, which is expected to be featured in the next-generation RAV4 SUV by March 2026. This system has been in development for seven years by Woven by Toyota, a subsidiary of Toyota, and is intended to boost vehicle connectivity through integrated telematics.

- The system will support over-the-air updates, advanced driver assistance features such as lane keeping and parking assistance, as well as enhanced infotainment capabilities. This initiative signifies Toyota’s strategic effort to upgrade its software capabilities and compete with leading companies in the connected vehicle technology sector.

Based on vehicle, the automotive OEM telematics market is divided into passenger cars and commercial vehicles. The passenger cars segment held a major market share of 71% in 2024 and is expected to grow significantly over the forecast period.

- Passenger vehicles, particularly hatchbacks, sedans, and SUVs, are quickly evolving into sophisticated connectivity centers. OEMs are incorporating telematics systems as standard features across these vehicle types to satisfy the increasing consumer demands. Even basic hatchbacks are anticipated to offer real-time connectivity. The ability to perform remote software updates and track performance has significantly improved service offerings, making embedded telematics crucial for delivering intelligent and seamless user experiences right from the point of delivery.

- Manufacturers are leveraging telematics data from sedans, hatchbacks, and SUVs to improve in-car experiences and develop new revenue streams. The ability to track driving behaviors, locations, and utilization in real-time allows car manufacturers to provide services such as predictive maintenance, insights into driving habits, and customized infotainment features.

- Luxury sedans might include AI-based coaching, while family-oriented SUVs could present entertainment features and safety alerts. This data facilitates usage-based insurance (UBI), geo-targeted marketing, and compatibility with third-party applications.

- Telematics installed by OEMs in passenger vehicles also aid in meeting regulatory requirements, particularly in regions where E call or vehicle tracking regulations are compulsory. These systems enhance customer satisfaction by providing proactive notifications, roadside assistance, and round-the-clock connectivity to support teams.

- Vehicle owners gain from immediate safety alerts, crash response services, and reassurance through smartphone applications. This enables OEMs to distinguish their brand and help in cultivating enduring loyalty. As governments progressively implement connected safety regulations, telematics is evolving into both a legal and commercial imperative in the passenger car market.

- For instance, in March 2025, BMW revealed a significant upgrade to its BMW operating System 9, which drives its newest lineup of connected passenger vehicles utilizing embedded telematics. This update improves personalization options, enables over-the-air updates and incorporates sophisticated safety services such as emergency response and adaptive driver assistance. The system is implemented in BMW IX, 5 Series and X1 models. By providing a smooth connected experience through factory-installed telematics, BMW is redefining its vehicles as not just modes of transport but as smart, adaptable digital partners.

Based on the application, the automotive OEM telematics market is divided into fleet/asset management, navigation & infotainment, vehicle diagnostics, safety & security, remote monitoring & control, emergency assistance (E call) and usage-based insurance (UBI). The fleet/asset management segment held a major market share of around 25% in 2024 and is expected to grow significantly over the forecast period.

- OEM telematics systems are now an essential part of fleet and asset management, providing commercial vehicle operators with the ability to track real-time locations, vehicle utilization, fuel efficiency, and optimize routes. This information empowers fleet managers to decrease downtime, manage operational costs effectively, and focus on driver safety.

- Automotive OEMs are incorporating sophisticated telematics solutions into their factory-installed systems, removing the necessity for aftermarket installations. This integration enables OEMs to provide bundled fleet management services directly, boosting customer retention and improving value-added services designed for logistics, ride-hailing and last-mile delivery companies.

- OEMs currently provide dashboards and mobile solutions that inform fleet managers about forthcoming service requirements, engine status or potential malfunctions before they result in breakdowns. These anticipatory insights not only decrease vehicle downtime but also enhance asset longevity. In fleet-centric sectors like logistics, mining, and public transport, this leads to substantial cost savings. OEMs are harnessing telematics to evolve from simple manufacturers to engaged service partners.

- Tracking driver behavior is a vital part of telematics in fleet management. Systems developed by OEMs accumulate data on braking, acceleration, idling and compliance with traffic regulations. This data can be analyzed to lower insurance claims, boost fuel efficiency and foster safer driving behaviors. The ability to track driving behaviors, locations, and utilization in real-time allows car manufacturers to provide services such as predictive maintenance, insights into driving habits, and customized infotainment features. Luxury sedans might include AI-based coaching, while family-oriented SUVs could present entertainment features and safety alerts.

- For instance, in January 2025, Ford pro upgraded its OEM telematics solutions for commercial fleets by launching Ford pro intelligence, which provides real-time insights into vehicle health, fuel usage, driver behavior, and predictive maintenance alerts. The platform interfaces directly with Ford’s factory-installed hardware, removing the need for third-party telematics. It targets logistics and service-oriented businesses looking to improve fleet performance and reduce operational costs. This solution exemplifies how OEMs are integrating telematics to transform into all-encompassing fleet management partners.

Based on connectivity, the automotive OEM telematics market is divided into 3G, 4G LTE, 5G and satellite communication. The 4G LTE segment held a major market share in 2024 and is expected to grow significantly over the forecast period.

- 4G LTE has emerged as the essential framework for telematics connectivity in contemporary vehicles, delivering a strong, low-latency network that facilitates real-time communication between vehicles and cloud services. OEMs incorporate these modules into vehicles to enable crucial functions like over-the-air (OTA) software updates, remote diagnostics, vehicle tracking and infotainment streaming. This provides significantly enhanced bandwidth and stability, leading to faster response times and smoother data flow.

- Across the globe, car manufacturers are integrating 4G LTE as the standard connectivity framework for their full range of vehicles, spanning from basic hatchbacks to luxury sedans and SUVs. This technology’s advanced features and wide-ranging network coverage make it the best selection for providing reliable telematics performance in different regions. Whether it involves safety alerts, navigation updates, remote locking or vehicle health diagnostics, 4G LTE ensures secure and fast data transmission.

- The industry’s move to 5G, 4G LTE still stands as the preferred choice for current OEM telematics solutions, due to its hard infrastructure and reliability. Most telematics service providers and vehicle platforms are optimized for 4G networks, ensuring a smooth user experience while minimizing the risk of operational disruptions. 4G LTE presents a swift and economical solution for engaging with connected services, bypassing the necessity to wait for the comprehensive rollout of 5G.

- For instance, In January 2025, General Motors verified that its Onstar telematics system, which is employed in Chevrolet, Buick, GMC and Cadillac vehicles, will keep operating on 4G LTE networks through at least 2030. This decision comes after the successful phase-out of 3G support and aims to guarantee continuous access to services such as automatic crash response, vehicle diagnostics, and remote access features. GM has indicated that 4G LTE provides the necessary bandwidth and reliability for its ongoing connected services and will remain the main connectivity solution as the 5G roadmap is gradually rolled out.

")

In 2024, the U.S. region in North America dominated the automotive OEM telematics market with 88% market share in and generated USD 10.5 billion in revenue.

- U.S. automotive manufacturers, including General Motors, Ford and Tesla, are achieving significant advancements in the incorporation of telematics by combining internal innovation with strategic technology collaborations. The Onstar system developed by GM and Ford’s Bluecruise serves as exemplary instances of fully integrated telematics systems that provide driver assistance, over-the-air (OTA) updates, vehicle diagnostics and connectivity services. Tesla continually excels in the management of vehicles through real-time software solutions. These OEMs have subscription-based approaches to monetizing data services, thereby converting telematics into reliable revenue streams.

- In the United States, changes in regulations initiated by the national highway traffic safety administration (NHTSA) and the federal trade commission (FTC) are influencing how OEMs handle telematics data. Concerns about data privacy and cybersecurity are growing, leading OEMs to be required to disclose their methods of collecting and using user data. There is a rising demand for right-to-repair and open data sharing policies. These evolving standards are urging OEMs to adopt transparent telematics frameworks that provide consumers with increased control over their vehicle data, while still enabling advanced services such as crash detection and driver behavior analytics.

- The telematics environment in the United States is bolstered by a robust technological ecosystem, which includes collaborations with prominent organizations such as Qualcomm, Amazon Web Services (AWS) and Google Cloud, all of which engage directly with automotive manufacturers. These partnerships are essential for enabling cloud-based telematics, data analytics and services driven by artificial intelligence. Companies such as SiriusXM connected vehicle services and Verizon connect assist OEMs in implementing infotainment, fleet tracking, and emergency response functionalities. The integration of telecommunications, AI, and automotive industries in the U.S. has fostered a vibrant and scalable environment, allowing automakers to swiftly deploy and advance connected vehicle technologies.

- For instance, in February 2024, General Motors (GM) revealed that beginning with the 2025 model year, every new Chevrolet, Buick, GMC and Cadillac vehicle will include the Onstar Basics package as standard. This package offers features like automatic crash response, remote vehicle commands and navigation and voice assistance, all provided at no extra charge for eight years. This initiative highlights GM’s dedication to improving vehicle connectivity and safety, in line with changing regulatory standards and consumer demands in the U.S. automotive telematics sector.

The automotive OEM telematics market in the Germany is expected to experience significant and promising growth from 2025 to 2034.

- The leading automotive original equipment manufacturers (OEMs) in Germany, including Volkswagen, BMW, and Mercedes-Benz, are spearheading the movement towards software-defined vehicles by incorporating state-of-the-art telematics in both electric vehicles (EVs) and internal combustion engine (ICE) models. These systems offer real-time diagnostics, predictive maintenance, and cloud-based infotainment, thus presenting advantages that surpass the initial sale of the vehicle. Brands are increasingly developing in-house software units, such as Volkswagen’s CARIAD, to control core telematics architecture. This OEM-centric model not only ensures deeper integration and faster updates but also supports Germany’s ambition to maintain a leadership role in connected and intelligent mobility.

- Germany implements rigorous data protection regulations in telematics, in accordance with the EU’s general data protection regulation (GDPR). OEMs are required to manage vehicle data, particularly personal or location-specific information with transparency and the consent of users. This regulatory framework has shaped the design of telematics platforms, promoting local data storage and improved encryption. German automotive manufacturers frequently collaborate with reliable European cloud service providers or develop their own proprietary systems. This compliance-oriented approach enhances consumer confidence and facilitates the scalable, secure deployment of telematics in both domestic and international markets.

- Germany boasts a robust automotive technology ecosystem, which includes suppliers such as Bosch, Continental, Elektrobit and Vector Informatik, all of whom are deeply involved in telematics innovation. These firms supply modules for vehicle communication, cybersecurity, over-the-air updates and vehicle-to-everything systems. Their persistent collaborations with OEMs ensure a fluid transition of research and development into telematics systems that are primed for production. The supplier network bolsters the integration of new protocols and standards, which is vital as the capabilities of telematics continue to evolve.

- For instance, in February 2025, CARIAD, which is the software branch of the Volkswagen Group, announced a collaboration with Bosch within the framework of the Automated Driving Alliance. The goal of this partnership is to establish a flexible and cost-efficient platform for assisted and automated driving across multiple vehicle segments. By using real-world driving data and agile development methods, the two companies are working toward scalable solutions that can be widely applied across Volkswagen’s global lineup.

- This initiative highlights Germany’s commitment to implementing cutting-edge telematics solutions while adhering to stringent data protection regulations. By merging CARIAD’s software expertise with Bosch’s hardware knowledge, the alliance showcases the robustness of Germany’s advanced automotive ecosystem in advancing telematics technology.

The automotive OEM telematics market in the China is expected to experience significant and promising growth from 2025 to 2034.

- The rapid advancement of EV technology in China is making a notable demand for telematics from domestic OEMs such as BYD, NIO and Xpeng. These firms are installing their vehicles with cutting-edge telematics systems that support real-time diagnostics, over-the-air updates, navigation, and driver-assistance capabilities. The commitment of the Chinese government to intelligent mobility, along with its encouragement of EV adoption, has significantly contributed to the extensive incorporation of vehicle connectivity features as standard provisions.

- In China, the telematics sector is shaped by rigorous regulatory supervision. The government mandates data localization, OEMs to retain vehicle-generated data within the nation’s borders. The “vehicle data security management provisions” are regulations aimed at ensuring that telematics systems comply with cybersecurity and user privacy standards. This requirement has led foreign OEMs to partner with local data providers or cloud service firms. Despite these legal constraints, they also boost swift progress for domestic telematics platforms by providing a secure environment for local companies such as Pateo and Navinfo.

- China’s telematics market is not solely driven by OEMs; it is bolstered by a vibrant ecosystem of local technology companies and startups. Firms like Banma (backed by Alibaba), Neusoft, and Tinnove (supported by Tencent) are creating in-vehicle operating systems and data platforms specifically designed for Chinese automotive manufacturers. Their offerings include capabilities like voice-activated controls, tracking of driver behavior, and predictive maintenance. These firms usually operate as Tier-1 or Tier-2 suppliers to OEMs, facilitating the rapid introduction of new telematics services into the marketplace.

- For instance, in March 2025, Leapmotor commenced pre-sales of its B10 SUV, marketing it as the least expensive electric vehicle in China that incorporates lidar and advanced telematics. The B10 is powered by Qualcomm’s Snapdragon 8650 chip and operates on a locally created smart cockpit system, consistent with China’s data localization policies. By depending on local suppliers and delivering real-time telematics, Leapmotor emphasizes the strengthening of China’s homegrown automotive technology landscape.

The automotive OEM telematics market in the Brazil is expected to experience significant and promising growth from 2025 to 2034.

- Brazil’s automotive OEMs are increasingly incorporating telematics as consumer demand for in-vehicle connectivity and safety features rises. Stellantis, GM, and Volkswagen are leading this change, introducing connected platforms in their popular models, especially in the compact and mid-range segments. Local consumers are welcoming features like emergency calls, real-time navigation, and vehicle diagnostics. To address the regional market, OEMs frequently partner with local telecom and IT companies, adapting services to fit Brazil’s infrastructure.

- Brazil’s national traffic department (DENATRAN) along with several regulatory bodies have promoted improved vehicle safety measures, which has consequently accelerated the integration of telematics. Anti-theft tracking systems are now mandatory in many vehicle types, turning telematics from a luxury option into an essential requirement. The government’s initiatives aimed at enhancing road safety and curbing insurance fraud are encouraging OEMs to incorporate telematics for crash reporting, monitoring driving behavior, and tracking fleets. This increasing synergy between policy and technology has fostered a conducive atmosphere for OEMs to provide telematics as either standard or optional features.

- Brazil’s telematics ecosystem is supported by strong local partnerships with telecom providers such as Vivo and Claro, which offer embedded sims and network support for connected cars. These partnerships allow OEMs to scale up telematics services with stable data transmission across urban and rural areas. Cloud platforms and local tech startups are also contributing by building apps and analytics dashboards tailored to Brazilian users. These players are helping to create a more localized and efficient telematics offering, positioning Brazil as a rising market for connected vehicle technologies in South America.

- For instance, in March 2024, Stellantis revealed a major investment in Brazil, announcing plans to launch 40 new vehicle models by 2030, which will include its inaugural hybrid cars. This initiative, totaling 6 billion dollars, emphasizes Stellantis’ dedication to innovation and sustainability within the Brazilian automotive industry. The investment aligns with Brazil’s federal Mover program, which encourages the use of environmentally friendly and safe vehicles, while also taking advantage of extended regional production incentives. Stellantis’ focus on developing hybrid and electric vehicles in Brazil highlights the nation’s growing significance in the global shift towards connected and sustainable mobility.

The automotive OEM telematics market in the Saudi Arabia is expected to experience significant and promising growth from 2025 to 2034.

- Under Saudi Arabia’s Vision 2030, connected and autonomous vehicles have been designated as a national priority, prompting OEMs to integrate advanced telematics into their regional offerings. The government is investing heavily in smart mobility infrastructure, particularly in progressive projects such as NEOM and The Line, which necessitate real-time vehicle connectivity and data-driven mobility solutions. These efforts are prompting OEMs such as Lucid Motors, Hyundai, and Toyota to adopt telematics systems that deliver navigation, remote diagnostics, and safety features specifically designed for the Saudi context and digital infrastructure initiatives.

- As logistics and commercial transportation are essential to Saudi Arabia’s economic diversification, the adoption of fleet telematics is experiencing significant growth. Businesses in the logistics, oil and gas and public transportation industries are implementing OEM-integrated systems for real-time vehicle tracking, monitoring driver behavior, managing fuel consumption and optimizing routes. Fleet operators in Saudi Arabia are progressively choosing connected vehicle services instead of aftermarket enhancements. This increasing demand for operational efficiency is prompting OEMs to include telematics as a standard feature in commercial fleets, establishing Saudi Arabia as a rapidly expanding market for B2B telematics.

- The telematics ecosystem in Saudi Arabia is advancing through strategic collaborations between OEMs, telecom operators like STC and emerging local tech enterprises. These partnerships concentrate on the integration of 5G, IoT and cloud solutions to support uninterrupted vehicle-to-cloud communication. The expansion of domestic electric vehicles and smart car manufacturing, propelled by firms like Ceer, is leading to the creation of new in-house telematics systems. OEMs entering the Saudi market are now required to adhere to local data regulations and telecommunications standards, necessitating a hybrid approach that combines global technology with local adaptations.

- For instance, in February 2025, Ceer Motors of Saudi Arabia, supported by the public investment fund and Foxconn, disclosed that its future electric vehicle lineup will add a fully integrated telematics platform designed in partnership with STC and local software companies. This platform will provide real-time diagnostics, monitor driver behavior, and enable over-the-air updates tailored for Saudi Arabia’s road and climate conditions. This initiative is in line with Vision 2030 and the drive for domestically produced smart vehicles, demonstrating how Saudi Arabia is merging government strategy, fleet requirements and local collaborations to establish itself as a regional telematics center.

Automotive OEM Telematics Market Share

- The top 7 companies of automotive OEM telematics industry are BMW Group, Ford Motor Company, General Motors, Hyundai Motor Company, Mercedes-Benz Group, Toyota Motor Corporation and Volkswagen, Group hold around 71% of the market in 2024.

- Connected drive by BMW enhances the driving experience with features like real-time navigation, over-the-air updates, and tailored concierge services.

It facilitates effortless interaction between the vehicle, the driver, and the cloud.With its integrated safety systems and advanced connectivity, connected drive showcases BMW’s commitment to providing a premium, data-enriched environment that meets the demands of luxury mobility and evolving driver expectations.

- The SYNC and Ford pass connect platforms from Ford deliver features such as voice commands, Wi-Fi, navigation, and app-driven vehicle controls. These functionalities facilitate real-time updates and remote access. By utilizing telematics, Ford enhances convenience and interaction across its gas and electric models, ensuring that driving is smarter, more intuitive, and better aligned with the everyday requirements of contemporary customers.

- GM’s OnStar system delivers safety, diagnostics, and remote services through real-time connectivity. It offers emergency support, vehicle monitoring, and proactive alerts. OnStar strengthens the link between car and owner, making GM a trusted name in telematics by prioritizing security, driver support, and consistent communication in daily mobility.

- Hyundai’s Blue Link system enables remote engine start, climate control, tracking, and diagnostics through an app. It is integrated into vehicles for immediate use and offers global accessibility. It enhances safety, convenience, and control, positioning Hyundai as a strong competitor in connected technology for both entry-level and luxury vehicle purchasers.

- Mercedes me connect allows for remote locking, vehicle monitoring and diagnostic insights. It merges intelligent functionalities with a touch of luxury, improving the overall appeal of luxury. Through tailored options and automation, the platform increases user satisfaction and strengthens Mercedes-Benz’s reputation as a leader in high-end connected vehicle technology.

- Toyota’s Safety Connect and Remote Connect offer emergency SOS services, remote engine capabilities and theft tracking. These systems are designed for both convenience and security by incorporating telematics across a diverse array of models, Toyota guarantees uniform safety features and promotes a customer-centric approach in the rapidly changing digital mobility environment.

- Volkswagen’s Car-Net and We Connect platforms deliver remote access, vehicle health updates, geofencing, and navigation tools. These features let drivers control car functions via smartphone. Volkswagen uses these telematics systems to boost efficiency, safety, and digital convenience, meeting modern expectations and contributing to smarter, connected driving ecosystems.

Automotive OEM Telematics Market Companies

Major players operating in automotive OEM telematics industry include:

- BMW Group

- Continental

- Ford Motor Company

- General Motors

- Hyundai Motor Company

- Mercedes-Benz Group

- Robert Bosch

- Tesla

- Toyota Motor

- Volkswagen Group

Prominent automotive manufacturers like BMW, Ford, and Mercedes-Benz are transforming the contemporary vehicle into a completely integrated digital ecosystem via their proprietary telematics platforms. BMW’s connected drive, Ford’s SYNC and Ford Pass Connect, along with Mercedes-Benz’s me connect, provide effortless access to services such as navigation, remote operations, emergency assistance and predictive maintenance. These platforms elevate the functionality of vehicles beyond just transportation, merging convenience, entertainment, and safety into the routine driving experience. Telematics has shifted from being a luxury to a vital strategy, empowering OEMs to distinguish themselves through personalized digital experiences.

Companies such as General Motors (OnStar), Toyota (Safety Connect, Remote Connect), and Volkswagen (Car-Net, We Connect) are utilizing telematics to facilitate the transition to software-defined vehicles. Featuring functionalities like remote diagnostics, over-the-air software updates, and voice-assisted control, these systems enhance vehicle intelligence and flexibility. This shift is not just about tech appeal it strengthens customer engagement, reduces dealership dependency, and provides an ongoing digital connection between OEMs and drivers. It also sets the foundation for more advanced services such as autonomous driving and usage-based insurance.

OEMs, Tier-1 suppliers such as Continental and Robert Bosch, are essential in enhancing telematics hardware and system integration. Electric vehicle innovators like Tesla are embedding telematics extensively within their ecosystems, improving aspects from route planning to battery diagnostics. Electric and software-defined vehicles gain popularity, the partnership between OEMs and technology suppliers is intensifying. Together, they are fostering advancements in connectivity, cloud integration and cybersecurity by transforming telematics into a fundamental component of future automotive mobility.

Automotive OEM Telematics Industry News

- In May 2025, Leapmotor, a producer of electric vehicles, adopted blackberry’s QNX platform for its new B10 SUV. Celebrated for its remarkable safety features and consistent performance, the QNX system will facilitate key functionalities in the vehicle, such as telematics, driver-assistance systems, and infotainment. This integration shows Leapmotor’s commitment to delivering intelligent and secure driving experiences. This decision illustrates Leapmotor’s dedication to providing connected driving experiences that are founded on a strong and dependable software infrastructure.

- In April 2025, L&T Technology Services (LTTS) secured a 50-million-euro agreement with a leading European automaker to develop and manage vehicle software for upcoming models. The project focuses on software-defined vehicle (SDV) platforms, proprietary operating systems, and cloud-based automotive technologies. LTTS will also establish a dedicated development center to support this initiative, reinforcing its position as a key player in global automotive software engineering.

- In November 2024, a comprehensive range of connected vehicle Software-as-a-Service (SaaS) solutions was launched by wireless cars on the AWS Marketplace. This initiative encourages automotive manufacturers to utilize digital tools for monitoring vehicle data, managing fleets, and delivering remote services. By harnessing the scalability of AWS cloud infrastructure, wireless cars are facilitating automotive enterprises in achieving their digital transformation targets.

- In November 2024, Rivian and Volkswagen Group initiated a joint venture named Rivian and VW Group Technology, LLC, backed by an investment of 5.8 billion dollars. The aim of this partnership is to jointly develop electric vehicles equipped with telematics and software-defined vehicle platforms. The effective use of Rivian’s software in a Volkswagen prototype showcases the potential benefits of this collaboration. This alliance merges Rivian’s cutting-edge technology with Volkswagen’s extensive production capabilities and scale.

automotive OEM telematics market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue (USD Million) and volume (units) from 2021 to 2034, for the following segments:

Market, By Type

- Embedded telematics

- Tethered telematics

- Integrated smartphone telematics

Market, By Vehicle

- Passenger cars

- Hatchbacks

- Sedans

- SUV

- Commercial vehicles

- Light commercial vehicles (LCV)

- Medium commercial vehicles (MCV)

- Heavy commercial vehicles (HCV)

Market, By Application

- Fleet/asset management

- Navigation & infotainment

- Vehicle diagnostics

- Safety & security

- Remote monitoring & control

- Emergency assistance (E-call)

- Usage-based insurance (UBI)

Market, By Connectivity

- 3G

- 4G LTE

- 5G

- Satellite communication

The above information is provided for the following regions and countries:

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Russia

- Nordics

- Asia Pacific

- China

- India

- Japan

- South Korea

- ANZ

- Southeast Asia

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- South Africa

- UAE

- Saudi Arabia