stockcam

Introduction & Investment Thesis

I initiated a “Sell” rating on Duolingo (NASDAQ:DUOL) on January 30th. My “sell” thesis was predicated on my belief that the stock was fully priced for future growth prospects. While the stock price initially declined approximately 10% after my “sell” thesis, it found support at the $170 price level, and since then, it is up close to 18%.

One of the main reasons behind the stock’s outperformance has been the company’s Q4 earnings report, which was released by the end of February. Since then, I have reassessed my thesis. I believe that I underestimated the company’s potential to expand its profitability in my valuation model in my previous “sell” rating, but after observing the management’s execution in FY23 and its projections for FY24, I am upgrading my rating to “buy.”.

The company exceeded both revenue and earnings expectations in Q4, with adjusted earnings per share (EPS) beating expectations by 66%. In FY23, Duolingo generated $531M in revenue, growing 44% YoY, while Adjusted EBITDA grew 500% YoY to $93.7M at a margin of 17.6%, compared to a margin of just 4.2% in FY22. This was driven by the company’s focus on driving product innovation, which improved the engagement on the platform as it saw its daily and monthly active users grow, while paid subscribers as a percentage of Monthly Active Users (MAUs) increased from 7.8% in FY22 to 8.3% in FY23, demonstrating the company’s success in attracting and engaging users, while optimizing its monetization on the platform and unlocking operating leverage. For FY24, Duolingo is expected to grow its revenue at a rate of 35–37% YoY to $717-$729M, while further improving its Adjusted EBITDA margin to a projected 22.5%.

Looking at both the “good” and the “bad,” I believe that there is a long-term opportunity for investors in this company with an upside of at least 24% from its current levels, making me upgrade my rating to “buy.”.

A quick primer on Duolingo

Duolingo is an innovative language learning app, and its mission is to develop the best education in the world and make it universally accessible. As of Q4 FY23, the company has a total user base of 88M MAU’s and it offers more than 40 languages. In FY23, the company also expanded its offerings to include math and music.

In terms of its business model, the company employs a freemium model. This allows users to access lessons without any cost while offering the option to subscribe to premium tiers that include Duolingo Super and Duolingo Max for an ad-free experience and extra features. The company generates 76% of its revenue from its subscription services, while the remaining 24% of its revenue comes from in-app advertisements, their widely accepted standardized English proficiency test called the Duolingo English Test, and in-app purchases.

Duolingo has differentiated itself by employing innovative gamified incentivization strategies where it offers tokens such as Streaks, Crowns, Gems. Leaderboards, and Heart to engage and motivate their users on the platform. The company prides itself on its culture of experimentation, so it can continue to innovate and improve their product and user experience.

The good: Outsized revenue and margin growth as accelerated product innovation drives user monetization

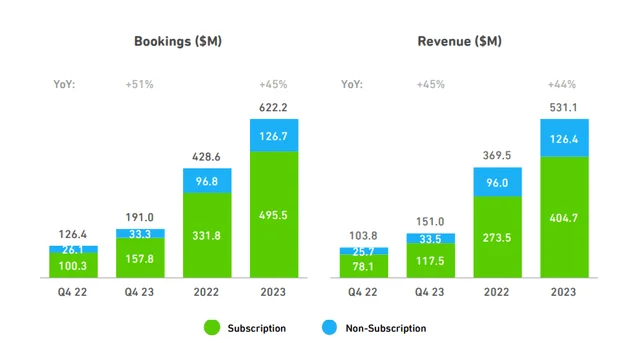

As of the latest earnings report, the company beat both its top- and bottom-line expectations. Duolingo’s revenue grew 45% YoY to $151M in Q4, while for the full year FY23, the company generated $531M, outpacing its prior year by 44%. In FY23, Subscription revenue grew 48% YoY, contributing 76% of Total Revenue. At the same time, revenue from in-app purchases grew 93% YoY in FY23 contributing 6.5% to Total Revenue, compared to 4.8% of Total Revenue a year earlier, which I believe is a testament that the company’s product innovation is on the right track, leading to highly engaged users on the platform.

Q4 FY23 Earnings Slides: Duolingo’s Revenue growth

Pivoting to Duolingo’s product innovation, I had talked about how Duolingo had expanded its offerings into new categories such as Maths and Music on its app in order to unlock new addressable markets to drive growth in my previous post. Meanwhile, the company continues to leverage generative AI to develop new features and lesson types that enable more conversational and listening practice, with the launch of DuoRadio in FY23, thus improving the overall user experience and engagement on the platform.

Looking into FY24, the management indicated that it will continue to invest in the product experience by iterating on its gamification strategies and building immersive lesson types to improve the conversion rate from freemium to paid subscribers as it further integrates AI into their products. At the same time, the company also indicated that it will experiment with pricing and the overall look and features of its three subscription tiers (free, Super, and Max) in order to optimize its user monetization on the app.

In FY23, the company saw its Daily Active Users (DAUs) and MAUs grow 65% YoY and 46% YoY to 26.9M and 88.5M, respectively. Paid subscribers also grew 57% YoY to 6.6M users. I believe this demonstrates that the management’s focus on product innovation to optimize its user conversion rate from freemium to paid is yielding the desired outcomes, as paid subscriber penetration as a percentage of MAU’s has improved to 8.3%, compared to 7.8% a year ago.

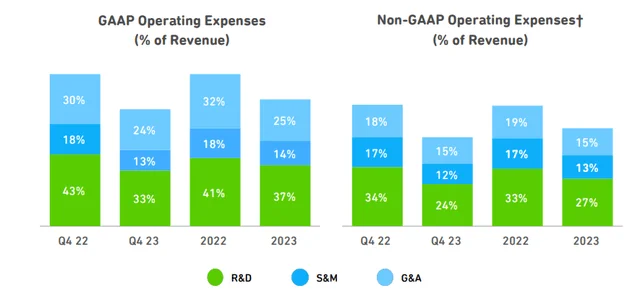

With users converting from freemium to paid at a faster rate, coupled with a higher volume of in-app purchases, has allowed the company to unlock operating leverage, as it saw its operating margins improve. Duolingo generated Adjusted EBITDA of $93.7M at a margin of 17.6%, a huge improvement from FY22, when Adjusted EBITDA margin was just 4.2%. At the same time, it also managed to streamline operating expenses that grew 20% YoY, while revenue grew at a much faster rate of 44% YoY, allowing Duolingo to expand its profitability.

Q4 FY23 Earnings Slides: Duolingo’s streamlining of operating expenses

Shifting gears to FY24 management guidance, the company expects to generate revenue in the range of $717M-$729M, which would represent a growth rate of 35–37%. At the same time, it expects to generate an Adjusted EBITDA of $154M-$171M, which would translate to a growth rate of 74% YoY at a margin of approximately 22.5%. This indicates that while the company is highly focused on driving rapid product innovation to engage and convert users to generate outsized revenue growth on its app, it is also remaining disciplined to expand its overall profitability, which I am thoroughly impressed by.

The bad: A global macroeconomic slowdown will hurt consumer spending, which will put pressure on Duolingo

In my previous post, I talked about how a possible slowdown in the US and the global economy could dampen Duolingo’s growth prospects. I still maintain that global macroeconomic uncertainty may pose a challenge for Duolingo, as it generates 47% of its total revenue outside of the US and the UK, leaving the company highly exposed.

We have already seen the UK economy slip into a recession earlier this year. Meanwhile, with inflation not decelerating at the pace that the US Fed would like, there is a growing probability of interest rates remaining higher for longer, which will in turn squeeze consumer discretionary spending in the US as the cost of borrowing remains elevated, coupled with a weakening job market. At the same time, major economies such as Germany and Japan are also in contraction territory.

It is important to note that the growth story of Duolingo is heavily connected to the robustness of consumer spending. Therefore, should we see a global macroeconomic slowdown, we can expect to see consumer spending dry up, which will hurt Duolingo’s growth prospects as it will experience a decline in conversion rate from freemium to paid subscribers as well as less volume of in-app purchases during that time.

Tying it together: Duolingo is a “buy”

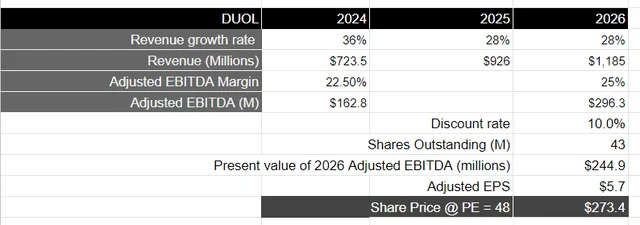

For FY24, Duolingo’s management guided revenue to grow approximately 36% YoY to $723M. At the same time, they also guided that Adjusted EBITDA will grow 74% YoY to $162.5M, representing an improvement in Adjusted EBITDA margin of 490 basis points to 22.5%.

Moving forward, over a 3-year time period, I will assume that the company will continue to grow its revenue in the high-20’s region, assuming there isn’t a prolonged period of a global macroeconomic slowdown. In that event, I believe that Duolingo should continue to maintain its pace of growth in the high-20’s region as it innovates its products to expand into new categories, thus expanding its TAM, while integrating AI to build improved and more personalized lessons and gamification strategies to drive a higher conversion rate and monetization of its user base. Simultaneously, given the management’s laser-sharp focus to expand its profitability, as it continues to streamline its operating expenses while improving user monetization, it should be able to grow its Adjusted EBITDA margin from a projected 22.5% in FY24 to an estimated 25% in FY26, resulting in approximately $296M in Adjusted EBITDA, or a present value of $244M, when discounted at 10%.

Taking the S&P 500 as a proxy, where its companies grow their earnings on average by 8% over a 10-year period with a price-to-earnings multiple of 15–18, Duolingo should be trading at approximately 2.75x the forward price-to-earnings multiple of the S&P 500 in FY26. That would translate to a forward price-to-earnings multiple of approximately 48, resulting in a price target of $273, an upside of 24% from its current levels.

Author’s Valuation Model

Conclusions

Although macroeconomic uncertainties remain a concern, Duolingo has thus far executed brilliantly, as it continues to drive rapid innovation that helps it attract, engage, and convert users on its platform. At the same time, the management is highly disciplined to ensure that it protects and expands its margins while maintaining the company’s growth story. As a result, I believe that the company is undervalued at current levels, with a possible upside of 24% over a 3-year investment horizon, making it a “buy” at current levels.