I’m not saying that working in digital media is some kind of picnic in 2024. Far from it, actually. But I am saying I’m glad I don’t work at Volkswagen or Stellantis right now.

Europe’s two largest carmakers are facing unprecedented headwinds this year. For Volkswagen, it’s endless software problems, labor woes, an inability to compete with China’s automakers on affordable and profitable EVs and the fact that its once-reliable Chinese presence has been almost completely devoured by the country’s homegrown newcomers. Volkswagen may even close plants in Germany for the first time in its nearly 90-year history.

For Stellantis—a kind of cobbled-together entity that consists of the former Fiat Chrysler group and PSA Peugeot Citroën, all with no discernable company culture connecting any of them—the list of problems has overlap with Volkswagen’s. But it’s also dealing with a series of misfires with brands like Jeep and Ram; American as they may be, they drive almost half the company’s revenue.

A much rosier view of the situation can be seen in a new report from the European NGO Transport & Environment (T&E), which says EVs are expected to reach 20% to 24% of new car sales in 2025. But when I read that, I have to wonder: Who is going to make those EVs?

Because from where we’re sitting right now, the answer increasingly feels like “China.” Or even “Chinese automakers who set up local factories in Europe.”

T&E’s latest analysis is a remarkably optimistic one, and I mean that not in terms of EV sales in general but for Europe’s automakers (and automakers that operate in Europe.) Currently, EVs make up about 14% of the European new car market, a number that has dwindled in recent months as subsidies to buy them disappeared.

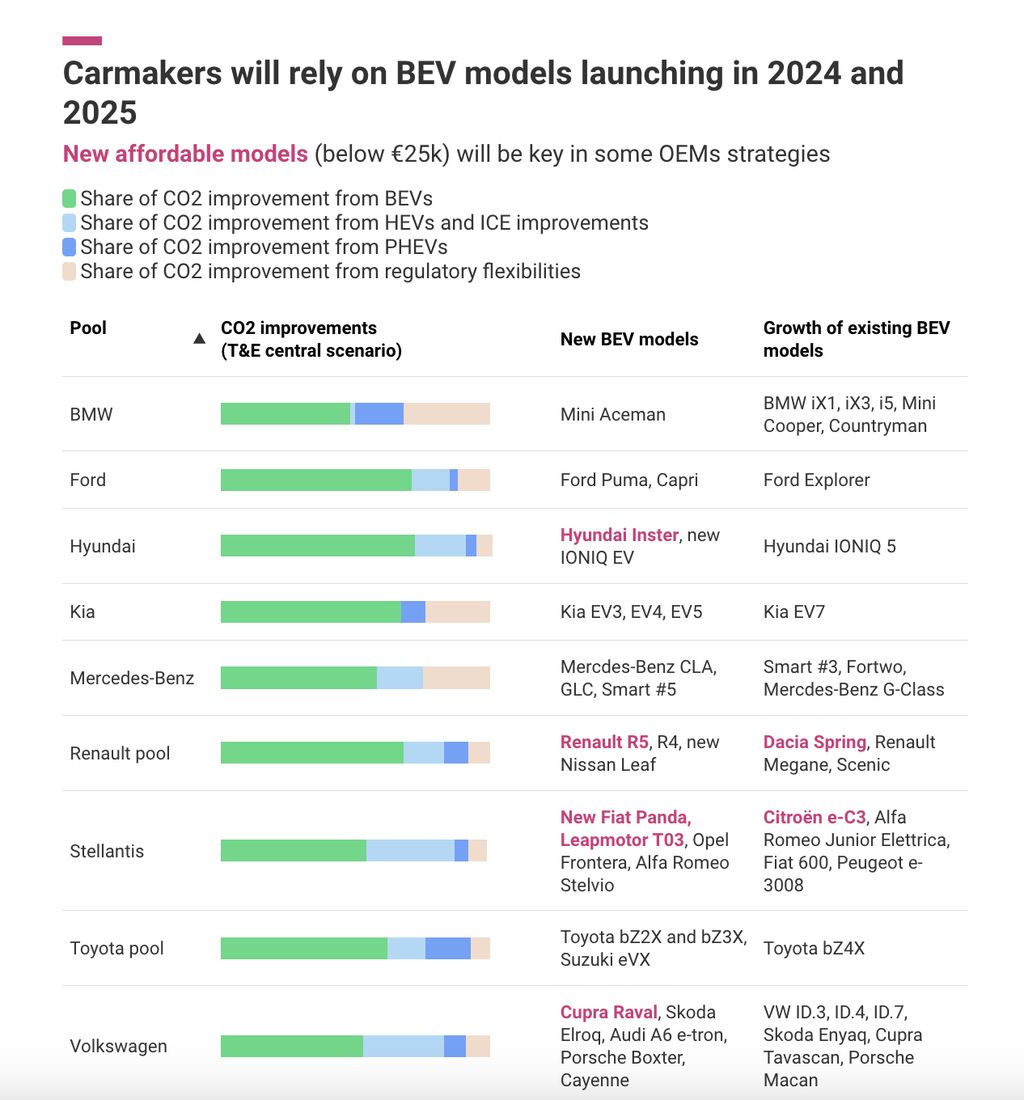

So this 6% to 10% jump in sales in a year is predicated on the glut of new, more affordable EVs coming to market in Europe in the next few months. “This will be partly driven by seven new fully electric models under €25,000 which have arrived or are coming on the market in 2024 and 2025,” T&E’s report said.

The predictions include many familiar makes and models, like the Mini Aceman; the Kia EV3, EV4 and EV5; the new Mercdes-Benz CLA-Class; the electric Ford Puma and Capri; and several new and updated models from the Volkswagen Group conglomerate.

Graphic: T&E

Mostly, however, I am stunned by the lack of Chinese automakers there, save for the Leapmotor T03 (which is being helped along by Stellantis.) Where’s MG on that list? Or Zeekr? Or Nio? Or XPeng? And perhaps most notably, where’s BYD? (I’d also argue this list should have Tesla on there somewhere since the Model 3 still led registrations in the first half of 2024, but I won’t get into the weeds there.) I’m also wondering how the slowdown in European battery factories will impact this projection.

We can be as dreamily optimistic as we want about Volkswagen’s EV comeback chances in Europe. But back in reality, the fact is that Europe’s automakers are not in a great place and not positioned well to compete with China’s EVs on costs.

That’s all on top of the fact that Europe’s car market has shrunk considerably in recent years. The kind of post-COVID economic recovery the U.S. has enjoyed—yes, even with all the inflation—has certainly not been the case everywhere.

“We are the largest manufacturer with around a quarter of the market share in Europe. We are short of around 500,000 cars, the equivalent of around two plants,” the Volkswagen Group’s CFO said recently. “The market is simply no longer there.” One piece of analysis from Just Auto indicates that Volkswagen, Stellantis and Renault may now have more than 30 factories between them operating at unprofitable levels.

However, one thing that will move that market again is the availability of much cheaper new models. And those will likely be from China or Chinese automakers, and if not hybrid or plug-in hybrid, then fully electric. It’s exactly what’s happening right now: Chinese brands made up to a record-high 11% of Europe’s total EV sales by June, but both those sales (and EV sales in general) have slowed as incentives dry up and new tariffs kick in.

Yet it’s expected to be a temporary slump. As Euronews noted this month, “Chinese car manufacturers are preparing to establish production plants overseas to counter the additional tariffs being imposed by other countries, which will likely boost their sales volume in the long term.”

Inside the BYD Atto 3.

Unfortunately, I don’t think we’re looking at any real “boosts” down the pipeline from Volkswagen or Stellantis. Next year will mark a decade since Volkswagen’s diesel cheating crisis led it to become the original “pivot to EVs” automaker. Since then, it’s merely led the way in proving how many of the assumptions around that move were wrong, like how much of the EV race depends on a battery supply chain largely controlled by China or how hard it is to get software right or how long China would be a buyer of foreign cars rather than a leading exporter of technologically superior ones.

And while some European buyers have proven as skeptical of Chinese cars as many Americans might be, time and time again, we see that prices are winning them over. Here’s Bloomberg, writing about a man in the UK who took the plunge and made his first electric car a BYD Atto 3, which undercuts a Tesla Model Y by thousands:

“It just goes,” says Kevin Wood, who lives in Hampshire, UK, and bought his first electric car last year. Wood, 54, took the leap of faith after discovering he could lease an EV through his employer, securing a tax break in the process. Then Wood took a second leap of faith: He chose an Atto 3, made by China’s BYD Co. Ten months later, he remains impressed by the SUV’s range, handling, comfortable seats, trunk space and voice-controlled sunroof. Wood calls it “genuinely a lovely car to drive.”

Expect more buyers to be won over the same way soon. And it’s hard to see much from Europe’s homegrown brands being able to outclass BYD’s combination of range, tech and above all, price.

On the American side of the pond, it may be tough to find sympathy for these automakers. Volkswagen has never felt especially relevant over here since its air-cooled heyday, and plenty of people are now wondering why Stellantis’ CEO gets paid $39 million a year to make cars that nobody is buying.

But above all, this situation feels like a warning—a preview of a level of pain that America just hasn’t felt yet. The European auto sector as a whole employs millions of people and many of those jobs, as well as the quality of life those jobs provide, feel more at risk than perhaps even during the Great Recession.

I don’t have any more of a prescription than anyone does for this problem. It seems hard to fathom a world where Volkswagen and Stellantis can compete with China’s draconian labor practices, or where any sane person would want them to try. But allowing European governments to end EV subsidies, back off their tough emissions targets and pray that anti-China tariffs will buy them time is not the same thing as making products that can meet or beat this new competition. And the climate crisis can’t wait for cleaner new cars, either.

“The car CO2 regulation has proven effective and will continue to push carmakers towards electrification but needs to be accompanied by national EV policies: charging masterplans and stable, targeted subsidy schemes,” T&E’s latest report said. “The current lead enjoyed by Chinese EV makers only shows that the longer the EU protects its laggard automakers, the less competitive they will be.”

But as you read this, the Belgian media is reporting that Audi may be in talks to sell its Brussels plant to China’s Nio. The way things are going, we may be reading variations on that headline for a long time to come.

Contact the author: [email protected]