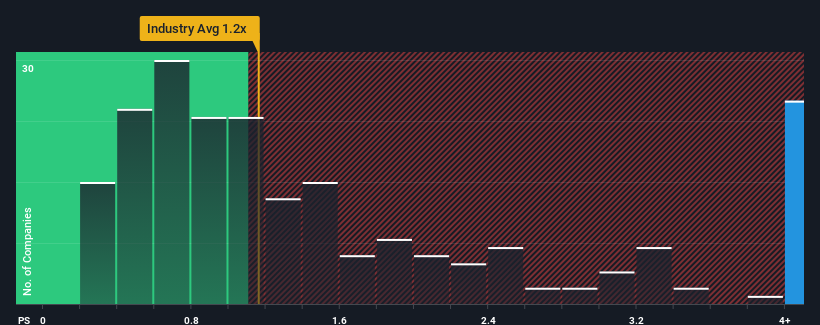

ENECHANGE Innovation Limited’s (TSE:4169) price-to-sales (or “P/S”) ratio of 5.9x may look like a poor investment opportunity when you consider close to half the companies in the IT industry in Japan have P/S ratios below 1.2x. Although, it’s not wise to just take the P/S at face value as there may be an explanation why it’s so lofty.

View our latest analysis for ENECHANGE Innovation

How ENECHANGE Innovation Has Been Performing

With revenue growth that’s superior to most other companies of late, ENECHANGE Innovation has been doing relatively well. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn’t the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think ENECHANGE Innovation’s future stacks up against the industry? In that case, our free report is a great place to start.

What Are Revenue Growth Metrics Telling Us About The High P/S?

ENECHANGE Innovation’s P/S ratio would be typical for a company that’s expected to deliver very strong growth, and importantly, perform much better than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 77% last year. The latest three year period has also seen an excellent 287% overall rise in revenue, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing revenue over that time.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 40% each year over the next three years. That’s shaping up to be materially higher than the 6.1% per annum growth forecast for the broader industry.

With this information, we can see why ENECHANGE Innovation is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From ENECHANGE Innovation’s P/S?

While the price-to-sales ratio shouldn’t be the defining factor in whether you buy a stock or not, it’s quite a capable barometer of revenue expectations.

We’ve established that ENECHANGE Innovation maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the IT industry, as expected. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless these conditions change, they will continue to provide strong support to the share price.

You should always think about risks. Case in point, we’ve spotted 2 warning signs for ENECHANGE Innovation you should be aware of, and 1 of them makes us a bit uncomfortable.

If you’re unsure about the strength of ENECHANGE Innovation’s business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we’re helping make it simple.

Find out whether ENECHANGE Innovation is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.