iMotion Automotive Technology (Suzhou) Co., Ltd. (HKG:1274) shareholders that were waiting for something to happen have been dealt a blow with a 66% share price drop in the last month. To make matters worse, the recent drop has wiped out a year’s worth of gains with the share price now back where it started a year ago.

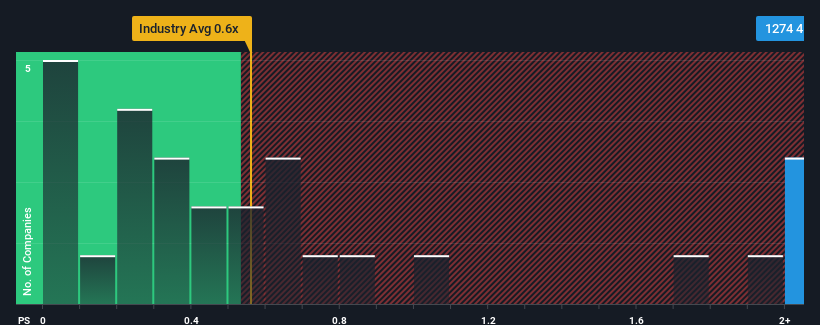

In spite of the heavy fall in price, when almost half of the companies in Hong Kong’s Auto Components industry have price-to-sales ratios (or “P/S”) below 0.6x, you may still consider iMotion Automotive Technology (Suzhou) as a stock not worth researching with its 4.6x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it’s justified.

Check out our latest analysis for iMotion Automotive Technology (Suzhou)

What Does iMotion Automotive Technology (Suzhou)’s P/S Mean For Shareholders?

iMotion Automotive Technology (Suzhou) hasn’t been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. Perhaps the market is expecting the poor revenue to reverse, justifying it’s current high P/S.. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on iMotion Automotive Technology (Suzhou) will help you uncover what’s on the horizon.

How Is iMotion Automotive Technology (Suzhou)’s Revenue Growth Trending?

iMotion Automotive Technology (Suzhou)’s P/S ratio would be typical for a company that’s expected to deliver very strong growth, and importantly, perform much better than the industry.

Taking a look back first, the company’s revenue growth last year wasn’t something to get excited about as it posted a disappointing decline of 8.3%. The latest three year period has seen an incredible overall rise in revenue, a stark contrast to the last 12 months. So while the company has done a great job in the past, it’s somewhat concerning to see revenue growth decline so harshly.

Shifting to the future, estimates from the two analysts covering the company suggest revenue should grow by 45% each year over the next three years. That’s shaping up to be materially higher than the 23% per annum growth forecast for the broader industry.

With this information, we can see why iMotion Automotive Technology (Suzhou) is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

A significant share price dive has done very little to deflate iMotion Automotive Technology (Suzhou)’s very lofty P/S. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We’ve established that iMotion Automotive Technology (Suzhou) maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Auto Components industry, as expected. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren’t under threat. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

You always need to take note of risks, for example – iMotion Automotive Technology (Suzhou) has 1 warning sign we think you should be aware of.

If strong companies turning a profit tickle your fancy, then you’ll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we’re helping make it simple.

Find out whether iMotion Automotive Technology (Suzhou) is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we’re helping make it simple.

Find out whether iMotion Automotive Technology (Suzhou) is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free Analysis

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]