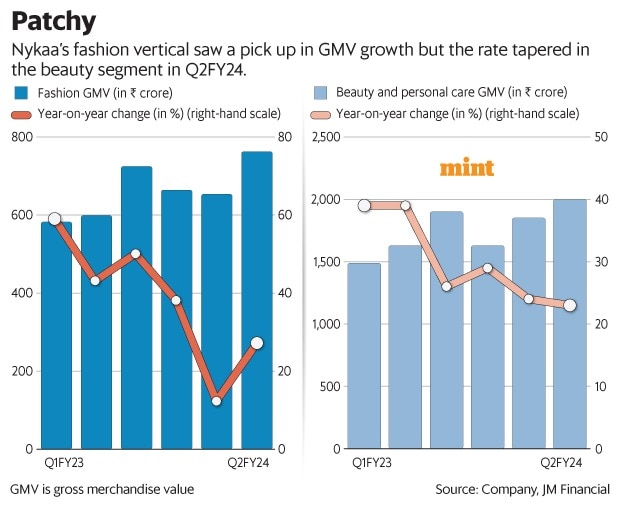

The relatively newer fashion business is finally adding oomph to FSN E-Commerce Ventures Ltd, the parent company of Nykaa. This vertical put up a strong show on the margin front in the September quarter (Q2FY24), thanks to premiumization, lower product returns and declining marketing expenses. As such, the fashion segment clocked a multi-quarter high contribution profit margin (as a percentage of net sales value) of 4.7%. In Q1, this measure stood at 2.7%. Contribution profit refers to gross profit after adjusting variable expenses such as fulfillment expenses, marketing costs and selling & distribution expenses.

")

View Full Image

What’s more, the fashion segment is expected to stay in vogue with better margin trajectory. This would be aided by an improving mix of existing customers and would lead to savings on marketing costs. Existing customers formed 46% of the fashion segment’s gross merchandise value (GMV) in Q2 versus 35% in the same period last year.

“We expect the segment to turn Ebitda profitable as contribution margin crosses 11%. It appears that the segment has turned a corner and is on track to generate incremental value for shareholders,” said analysts at JM Financial Institutional Securities in a report on 6 November. Ebitda, a measure of profitability, is short for earnings before interest, tax, depreciation and amortization.

However, it is not a pretty picture as far as Nykaa’s mainstay beauty and personal care (BPC) segment is concerned. Competition is heating up in this category, led by direct-to-consumer brands as well as international brands that operate on Nykaa’s platform. In a bid to hold on to market share, the brands are offering additional discounts, which is weighing on Nykaa’s margin. Further, ad revenue is yet to rebound even though it has shown sequential improvement in Q2. Also, the shift in the festive season by almost 20 days had some impact on BPC’s GMV growth in Q2, which was 23% year-on-year—the second consecutive time of drop in the growth rate.

The upshot: BPC’s contribution margin fell by 20 basis points (bps) year-on-year to 26.4%. The margin outlook is not particularly encouraging. Analysts at Elara Securities (India) note that savings in fulfillment cost and marketing expenses have largely peaked in BPC. The brokerage does not expect any sharp improvement in the segment’s profitability on the back of increased competition from quick commerce players and platforms such as Tira. Tira is an omnichannel beauty retail platform under Reliance Industries Ltd.

But there are bright spots. The BPC segment’s average order value is up by more than 2% year-on-year to ₹1,916, indicating an improvement in the quality of transactions and customer groups. Also, the mix of existing customers in BPC’s GMV is healthy. Further, tailwinds in Q3 from the festival season and the Hot Pink sale in November would boost BPC’s GMV.

Meanwhile, Nykaa’s Other business continues to be in the red at the contribution profit level. This includes NykaaMan, e-B2B platform – SuperStore by Nykaa, international brands, Little Black Book and Nudge. Here, the e-B2B business is seeing an improvement in the contribution margin and that is a positive. As the businesses gain scale, the loss is likely to narrow.

To be sure, the progress towards profitability in the fashion business is a key monitorable and may aid investor sentiment. In this calendar year so far, the Nykaa stock is down by nearly 4%.

“Consistent improvement in profitability in fashion and lower losses in e-B2B may drive multiple re-rating for Nykaa,” said the Elara report dated 6 November.